Argyle helps First United cut verification spend by 65%.

Restoring point-of-sale verification while strengthening long-term partnership value

About

Family owned, family operated and built on family values, First United Bank (First United) is one of the largest privately held community banking organizations in the United States. Established in 1900, First United holds approximately $16 billion in assets and serves customers across Texas and Oklahoma at more than 80 locations. Its distributed retail mortgage operating group employs roughly 100 loan officers, with operations centralized in Plano, Texas.

Challenge

For years, First United utilized third-party verification solutions as a core part of its mortgage process. These solutions were reliable and required minimal day-to-day oversight as the business scaled.

Over time, however, verification costs increased significantly as loan volumes and market conditions evolved. What had once been a low-friction part of the process became a meaningful expense, prompting the team to reassess how and when verifications were ordered.

“We pushed a lot of verification to the point of sale at a time when it cost $20 to $25 per file,” says Gerrin Chenault, vice president and director of project administration and mortgage systems at First United. “It was easy to set it and forget it. Then one day, you open your invoice and realize how quickly those costs have added up.”

To better manage spend, First United implemented guardrails around verification requests—centralizing ordering and tying usage to defined criteria. While this improved cost control, it introduced a tradeoff: verification shifted later in the loan process, reducing early borrower engagement and self-service opportunities.

The team’s goal was clear—restore verification to the point of sale to reduce friction, strengthen pre-approvals, and improve pull-through—without reintroducing unsustainable costs.

.avif)

Solution

First United first encountered Argyle at ICE Experience, where the team saw a live demonstration of the platform’s automated, payroll-based verification of income (VOI) and verification of employment (VOE). A key requirement was already met: Argyle’s native integration with Encompass®, the bank’s loan origination system.

Following additional evaluation, First United selected Argyle as a long-term strategic partner to modernize verification—combining seamless system integration with a pricing model that supports point-of-sale adoption.

“It became clear this was the right move, and we haven’t looked back,” says Jeff Meuschke, vice president and director of enterprise solutions at First United.

A critical next step was embedding verification directly into the bank’s point-of-sale platform, LiteSpeed from LenderLogix. Through close collaboration, Argyle, First United, and LenderLogix partnered to fast-track an integration that places VOI and VOE directly within the borrower needs list. Verification requests and results flow seamlessly back into Encompass, maintaining a single system of record.

This collaborative approach not only accelerated implementation but also established a strong foundation for continued innovation between First United and Argyle.

Outcome

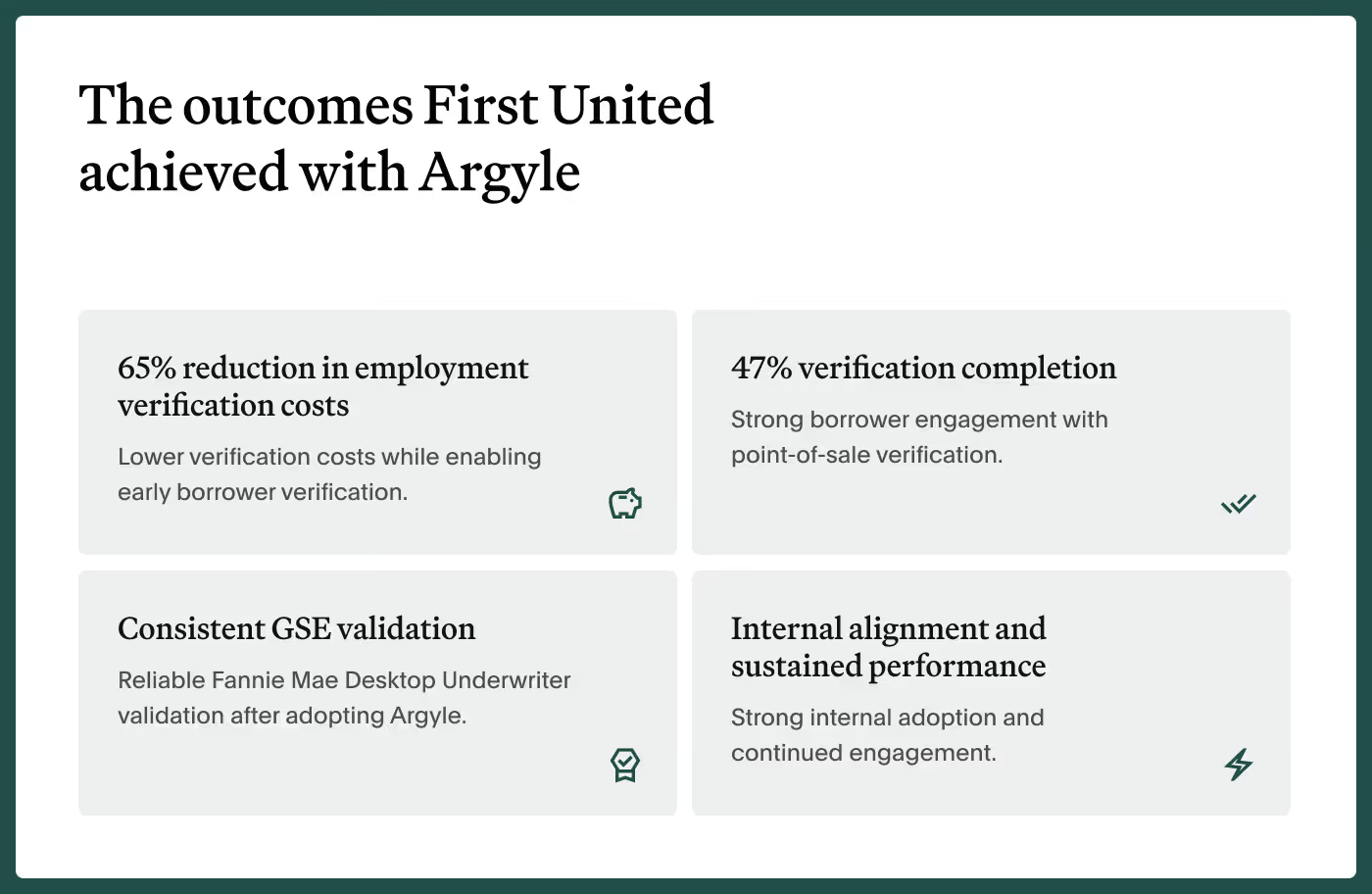

65% reduction in employment verification costs

Within months of implementation, First United significantly reduced verification spend—lowering monthly costs from approximately $125,000 to under $40,000.

With a more sustainable cost structure in place, the bank can confidently present VOI and VOE to borrowers at the very start of the application process.

“We feel comfortable putting payroll-based VOI and VOE in front of every borrower,” Chenault says. “At Argyle’s price point, even if more than half complete the verification, the economics still make sense.”

47% verification completion

By reintroducing verification at the point of sale, First United now offers the experience to nearly every applicant—whether they are early-stage prospects or active buyers.

Even with this broad approach, verification completion reaches 47% in peak months, reflecting strong borrower engagement when introduced early in the journey.

“Once we put verification in front of borrowers early, the engagement followed,” Chenault says. “Seeing that level of completion consistently month over month reinforced that we made the right decision.”

Consistent GSE validation

Moving verification earlier in the process did not impact secondary market performance. First United continues to receive consistent income and employment validation through Fannie Mae’s Desktop Underwriter, with no decline in Day 1 Certainty results.

“As a bank with around 60% of our production going to the GSEs, maintaining consistent DU results was critical for us,” Chenault says. “Argyle has met that bar.”

Internal alignment and sustained performance

First United continues to partner closely with Argyle to monitor performance, optimize borrower engagement, and expand use cases over time.

Not long after implementation, members of the sales team proactively sought additional information to better position the new verification experience with borrowers—an indicator of strong field adoption.

“That’s meaningful to me because we don’t often have sales teams asking for more of a system we’ve implemented,” Chenault says. “It tells us the change is resonating in the field.”

Looking ahead, First United and Argyle are aligned on expanding capabilities beyond VOI and VOE—including asset verification and document-based income verification—further enhancing the borrower experience and operational efficiency.

“With Argyle in place, we’ve been able to rethink how verification fits into the borrower experience today and how it can evolve going forward,” Meuschke says.

.avif)

Ongoing Partnership & Governance

As First United continues to expand its use of Argyle, both teams remain committed to ongoing collaboration, performance optimization, and innovation across the borrower journey.