How Doc VOI Solves the Last Mile of Verification for Applicants Who Can’t Connect

Successfully closing automation gaps in the verification waterfall

Every digital verification strategy faces a gap sooner or later. Even with Argyle’s industry-leading 55% average conversion rate for direct payroll connections, there’s always a small portion of applicants who can’t or won’t successfully connect their accounts.

Maybe they work for an employer whose payroll platform isn’t supported by our extensive network, which covers 90% of the U.S. workforce. Or maybe they simply prefer submitting their financial documents themselves. Whatever the reason, these applicants have historically been excluded from automated verifications, forcing them (and the providers that serve them) into slow, manual workflows that drive down completion rates and compromise the application experience.

Doc VOI closes that gap by automating document-based income verifications with the same speed and reliability as direct-source connections. This ensures every applicant can move through the verification process efficiently regardless of their ability or willingness to connect their accounts.

In this post, we explore how Doc VOI completes the verification waterfall, how providers and applicants benefit from automated document processing, and how this transforms verification economics for forward-thinking financial service organizations.

The missing piece in the verification waterfall

The most effective verification strategies follow a waterfall approach, starting with direct-source payroll and banking connections and only resorting to alternative methods when those processes fail. The problem has always been what happens at the bottom of that waterfall, when automated options appear to run out.

Before Doc VOI, providers that couldn’t connect applicants directly faced one of two possibilities:

- Manual document review

They could ask applicants to find, scan, and submit their paystubs, W-2s, and other financial documents by hand. Their team would then spend hours combing through these files, calling or emailing employers to verify the details, and engaging in endless back-and-forth until all required income and employment information was complete and accurate. This process would prove to be slow, costly, and inconsistent, introducing untold delays and human errors into the verification flow.

- Expensive legacy databases

Alternatively, providers could purchase verification reports from legacy databases like The Work Number (TWN). These static reports often contain outdated data, and they don’t include access to essential documents like paystubs and W-2s, meaning providers still need to rely on manual document collection and review. Moreover, TWN reports come with a steep price tag, often running upwards of $200 apiece. If (or when) providers need to reverify an applicant, they’re forced to purchase another full-price report and repeat manual tasks. This adds cost and stress without delivering the real-time accuracy or data quality that direct-source connections supply.

Neither backup option works well by modern standards. Applicants are left waiting, verification teams are buried in time-consuming paperwork, and important business decisions are stalled, with delays frequently driving applicants to abandon their application and look elsewhere.

Solutions like Argyle’s Doc VOI change that dynamic. By automating document-based verifications with the same speed and reliability as direct-source connections, they ensure every applicant can move through the verification process efficiently and effectively.

How Doc VOI works

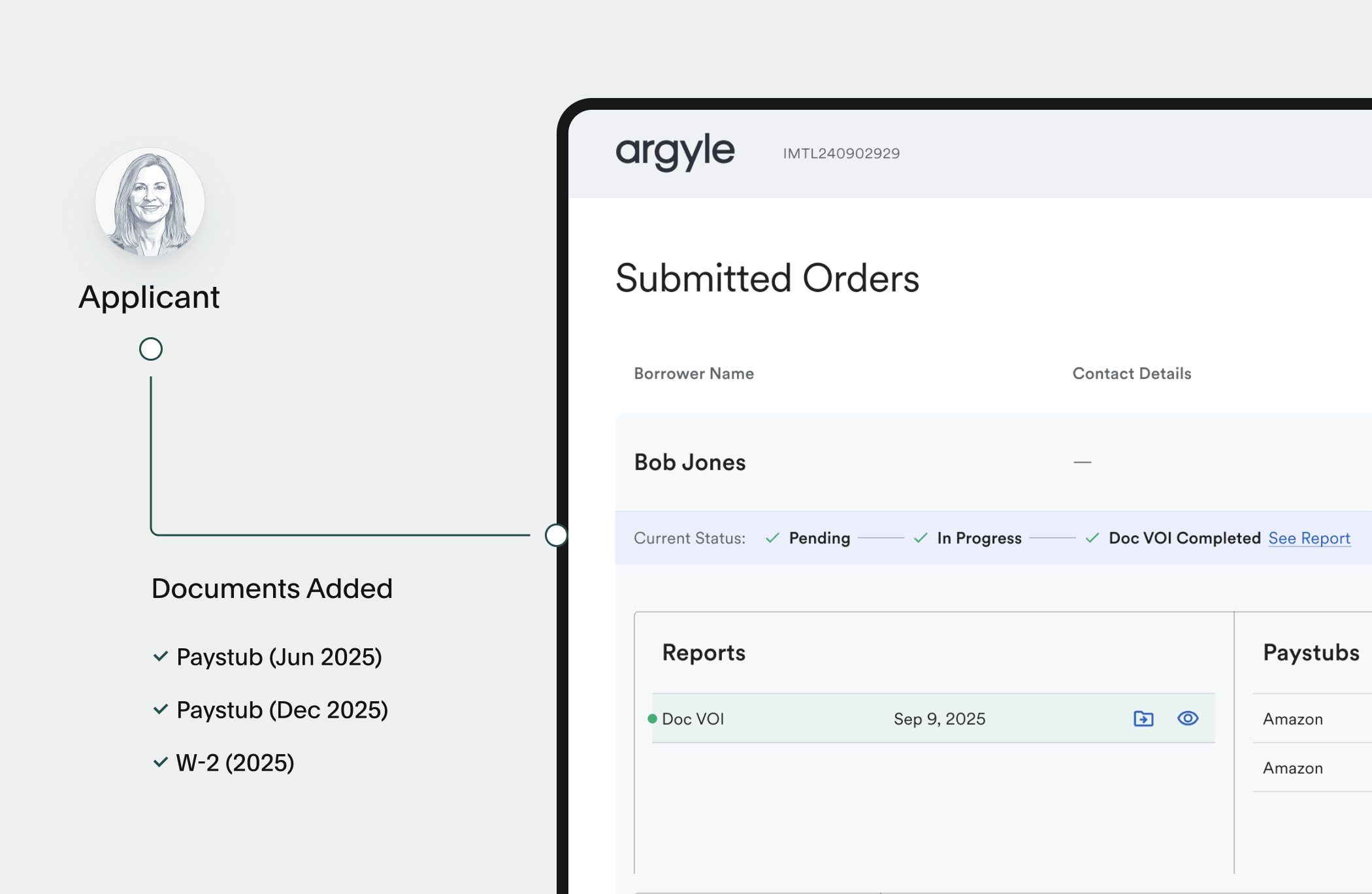

Doc VOI uses advanced optical character recognition (OCR) technology to extract income and employment data directly from uploaded paystubs, W-2s, and other proof-of-income documents. That data is then returned as a clear, structured verification report within a matter of minutes.

For mortgage lenders using Encompass® as their loan origination system (LOS), documents and Uniform Residential Loan Application (URLA) information are retrieved directly from the Encompass eFolder, using Doc VOI. For providers with proprietary systems, Doc VOI integrates via the Argyle API, allowing applicants to upload documents through an existing interface. Either way, the process is seamless. Documents are automatically processed, data is quickly extracted and standardized, and verification reports are generated without manual intervention.

That means no waiting for team members to manually review documents, no back-and-forth with applicants to clarify and fill missing fields, and no delays that push applicants away to faster-moving competitors.

This is the “last-mile” solution that providers have been waiting for: a way to automatically verify applicants who fall outside direct-connect solutions, eliminating the gap that has historically forced them into manual processing queues or expensive database queries.

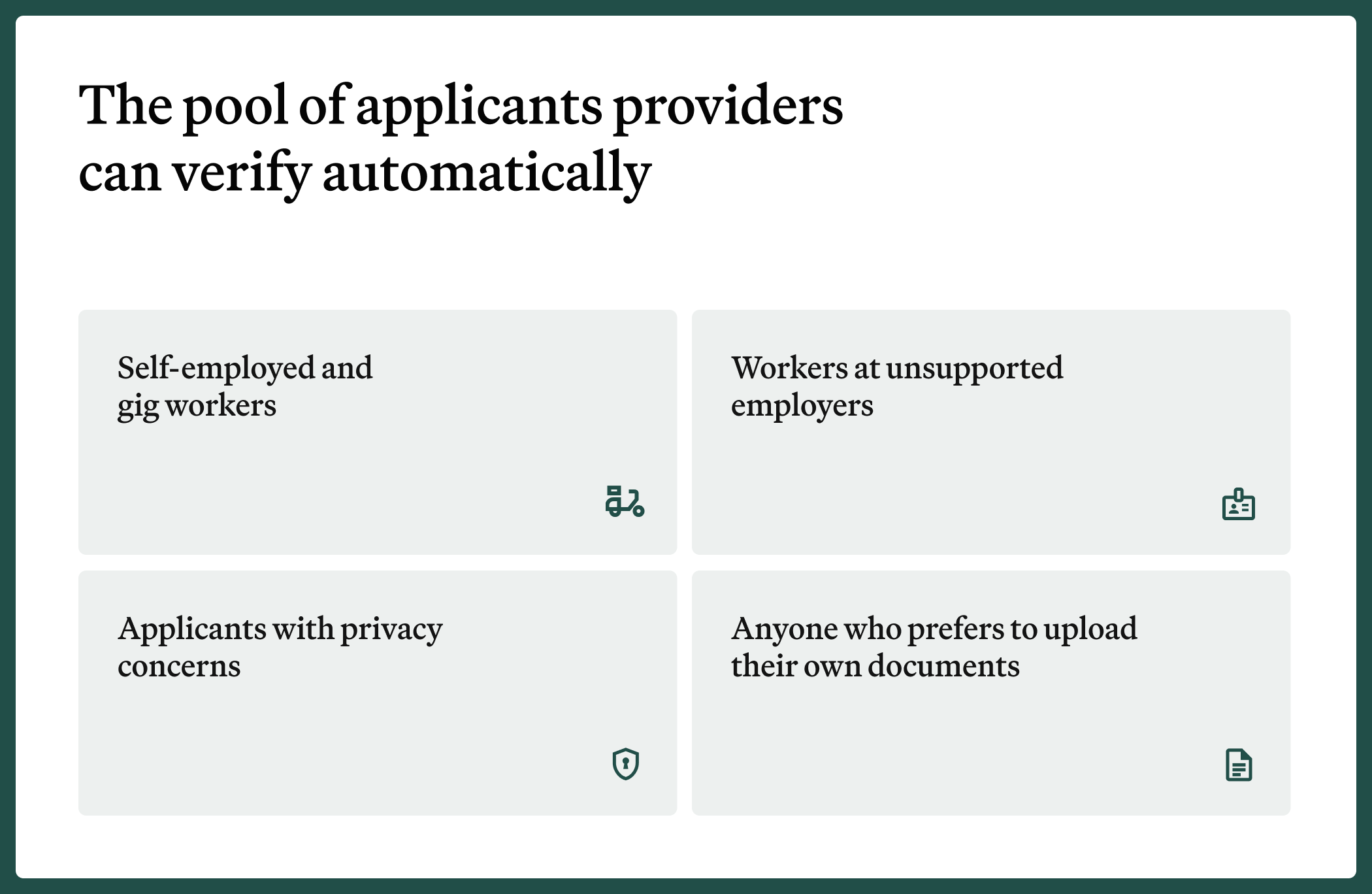

Expanding the verifiable applicant pool

By providing a fast, reliable backup or alternative to direct-source connections, Doc VOI captures applications that would otherwise require manual processing, dramatically expanding the pool of applicants providers can verify automatically. This includes:

- Self-employed and gig workers: Applicants with multiple income streams from nontraditional sources like Uber, DoorDash, or freelance work can quickly upload proof-of-income documents to verify all of their earnings. Instead of requiring multiple tools or manual steps to verify each source of income, Doc VOI processes their documents together in one streamlined flow.

- Workers at unsupported employers: Even with Argyle’s 90%+ workforce coverage, there will always be edge cases and exceptions. Doc VOI ensures those applicants don’t get left behind.

- Applicants with privacy concerns: Some applicants simply aren’t comfortable inputting their account details, while others may have lost or forgotten their credentials. Doc VOI gives them an automated alternative that respects their preferences and enables them to verify their income with the documents they have on hand.

- Anyone who prefers to upload their own documents: Most importantly, it’s vital to give applicants a choice in the verification process. Argyle’s Doc VOI solution allows them to verify their way without compromising on speed or accuracy.

Transforming verification economics

For financial service providers across industries, from mortgage lenders and personal lenders to tenant screening providers, Doc VOI offers substantial business benefits. These include:

- Greater efficiency: Automated document analysis and OCR technology reduce manual review backlogs, preventing bottlenecks that slow down application pipelines and freeing up verification teams to focus on more strategic, higher-value work.

- Cost savings: Providers can reduce verification expenses by up to 80% compared to expensive legacy solutions like databases and manual reviews.

- Higher approval volumes: By automating document-based verifications that would otherwise fall through the cracks, Doc VOI expands the share of applications that can be processed efficiently and accurately without expanding risk exposure.

- Built-in GSE compliance: Argyle’s Doc VOI solution integrates fully with Freddie Mac’s Asset and Income Modeler (AIM) Check—a capability within Freddie’s Loan Product Advisor® (LPA®)—allowing mortgage lenders relief from reps and warrants on income calculations using payroll documents.

- Early qualification: Mortgage lenders can confirm AIM-qualifying monthly income before submitting to LPA, accelerating the underwriting process and improving the applicant experience.

As an example, NFM Lending had already embraced digital verifications but found many third-party verification vendors to be limited and costly. Their team was forced to pay higher prices year over year while still relying heavily on manual document processes. After adding Argyle’s Direct-Connect Payroll and Doc VOI solutions to their waterfall, NFM saved 80% on total verification costs, accelerated close times by an average of 10 days, and saw conversion rates surge to a projected 75%.

Including Doc VOI in our verification process gives us confidence that we can quickly qualify borrowers using documents when needed. This flexibility ensures a smooth borrower experience and supports timely processing.” — Cindy Keith, Chief Strategy Officer at NFM Lending

Similarly, Compass Mortgage faced verification costs that routinely climbed into the $200–$300 range per loan file with legacy providers, along with data accuracy issues that required time-consuming follow-ups with applicants’ employers. After implementing Argyle’s verification waterfall—including Doc VOI for applicants who can’t connect directly—Compass reduced their verification costs by 43%, increased conversion rates 17% (from 41% to 58%), and achieved AIM validation on 37.5% of document-based verifications, securing valuable relief from reps and warrants.

Seeing early AIM validations through Doc VOI is a big win for us. More borrowers are completing income and employment verification successfully. That improvement in follow-through has been one of the most noticeable changes for our team.” — Nicki Cather, Senior Vice President of Loan Operations at Compass Mortgage

.png)

What Doc VOI means for applicants

From an applicant’s perspective, Doc VOI removes a major pain point. Instead of being told they need to wait days or weeks for manual reviews to wrap up, they enjoy quick, accurate answers and a smooth process.

In other words, Doc VOI respects how people want to verify their income while ensuring they don’t get penalized with slower processing or manual workarounds because of how they choose to earn a living. That’s the kind of experience that builds trust and keeps applications from churning midstream.

Completing the verification waterfall

With Doc VOI, Argyle now capably covers every step of a full-scale verification waterfall:

- Direct-source, consumer-permissioned payroll connections cover 90%+ of the U.S. workforce and yield real-time, ongoing access to essential income and employment data and documents.

- Direct-source, consumer-permissioned banking connections cover 95%+ of direct deposit accounts and yield real-time, ongoing access to essential assets data and documents.

- Document processing (Doc VOI) with OCR technology automates income verification from seamlessly uploaded, digitally processed payroll documents like paystubs and W-2s.

By unifying automated payroll connections, banking connections, and document processing in a single platform, Argyle enables financial service providers to run their entire verification waterfall through a single partner, delivering greater consistency, cost savings, and conversions.

Instead of piecing together solutions across multiple methods and vendors, everything is handled through Argyle with one integration, one interface, and one source of reliable, high-quality data.

Getting started with Doc VOI

Doc VOI is available now as part of Argyle’s comprehensive verification platform. It integrates with Encompass and connects via the Argyle API for organizations using other LOS or proprietary platforms. That means teams can work directly within the systems they already use with no workflow disruptions or learning curves.

If you’re looking to close the gaps in your verification waterfall and ensure every applicant gets a fast, frictionless verification experience, Doc VOI delivers the perfect solution. Get in touch with our expert team to see how it can take your verification flow to the next level.