2026 Must-Haves for Mortgage Lenders: Automated, Embedded, Consumer-Permissioned Verifications

The mortgage market in 2026 remains fiercely competitive, with lenders navigating a landscape of compressed margins and elevated operational costs. In recent quarters, the average production profit margin was 33 basis points compared to the long-term average of 40 basis points. Meanwhile, average per‑loan production costs reached $11,109—well above the historical long-term average of $7,799.

In this environment, operational excellence will be critical, and efficient income, employment, and asset verification workflows will be a defining competitive advantage. According to an industry survey, 93% of mortgage processors still verify income manually at least 10% of the time, while more than one-third report growing dependence on manual methods. The lenders that win in 2026 will be those that instead prioritize automated, embedded, real-time verification infrastructure.

Here's what that looks like in practice.

Must-have #1: end-to-end automation that eliminates manual touchpoints

The days of manual verification workflows—chasing paystub uploads, making employer callback attempts, and managing email follow-ups—are numbered. These processes simply don't scale in a market where borrowers expect instantaneous digital experiences, and speed determines whether a lender closes a loan or loses it to a competitor.

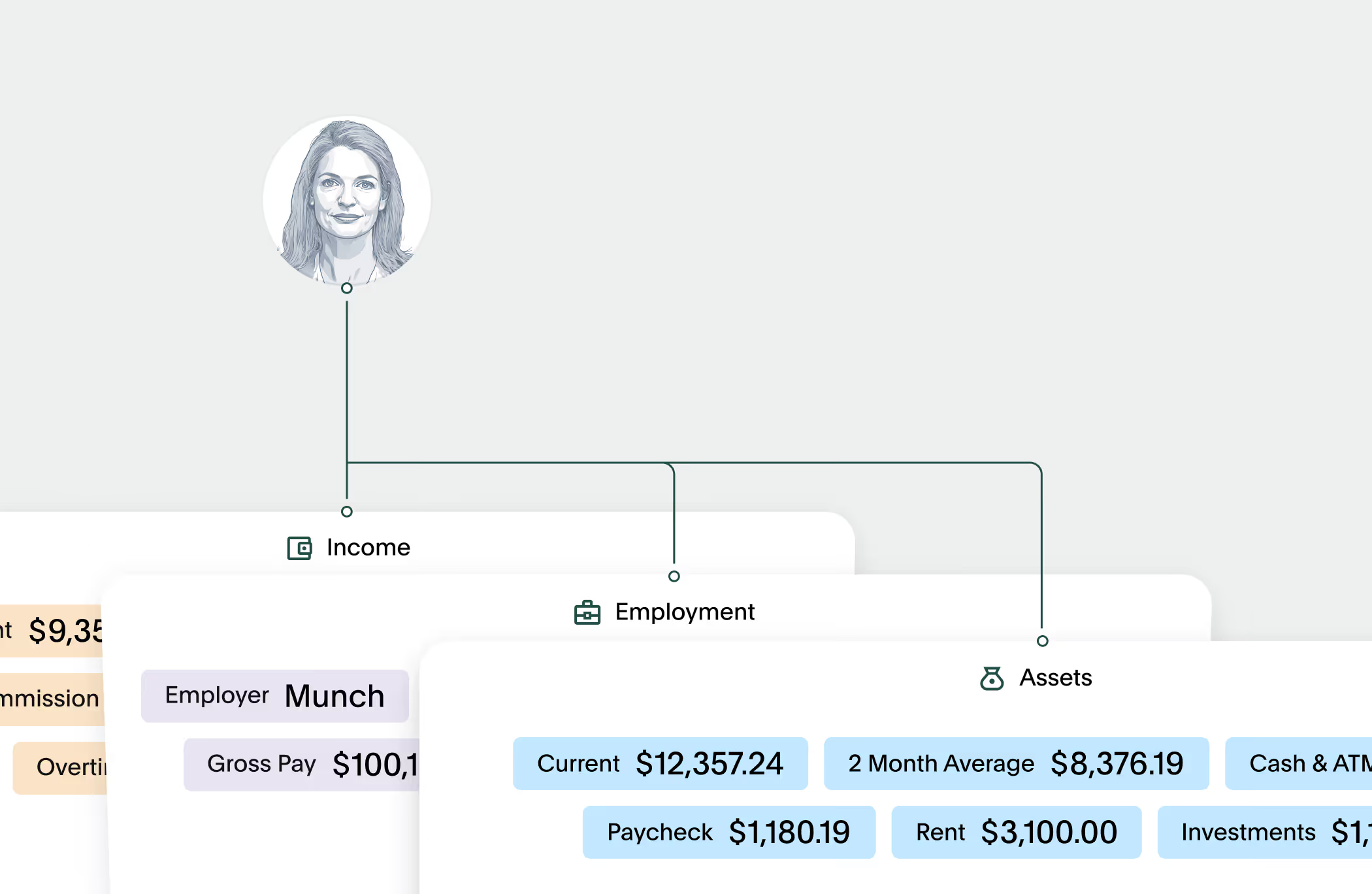

[design callout] Automation via a direct-source, consumer-permissioned verification provider is the answer. By connecting lenders’ back-office systems directly to borrowers’ payroll or banking accounts, lenders get real-time income, employment, and asset data, plus documents like paystubs and tax forms, straight from the source of truth.

This benefits lenders’ bottom line in measurable ways:

- Direct-source, consumer-permissioned verifications eliminate the delays caused by manual document collection.

- They prevent the submission of incorrect, incomplete, or fraudulent documents that slow down traditional manual reviews.

- In turn, they dramatically improve timelines and lower costs per verification.

Argyle's platform exemplifies the direct-source, consumer-permissioned approach to automation. With Argyle, lenders receive verification reports instantly when borrowers establish payroll or bank connections, providing reports, documents, and datasets fast, without the legwork of manual workflows.

The advantages aren’t just theoretical. Leading lenders like NFM Lending credit Argyle with 80% lower verification costs and timeline reductions of 10-12 days from application to clear-to-close.

Must-have #2: moving verifications to the POS to transform lender economics

One of the most significant shifts happening in 2026 is the migration of verifications from loan origination systems to point-of-sale systems. It’s a change that fundamentally transforms both the borrower experience and lender economics.

That’s because POS-based verification workflows make verification an effortless part of the initial application flow—when borrower engagement peaks—rather than a later burden. This not only leads to higher completion rates, it also results in more GSE-eligible verifications by securing quality data upfront. As a result, they deliver less risky loans and greater cost savings compared to LOS-triggered workflows.

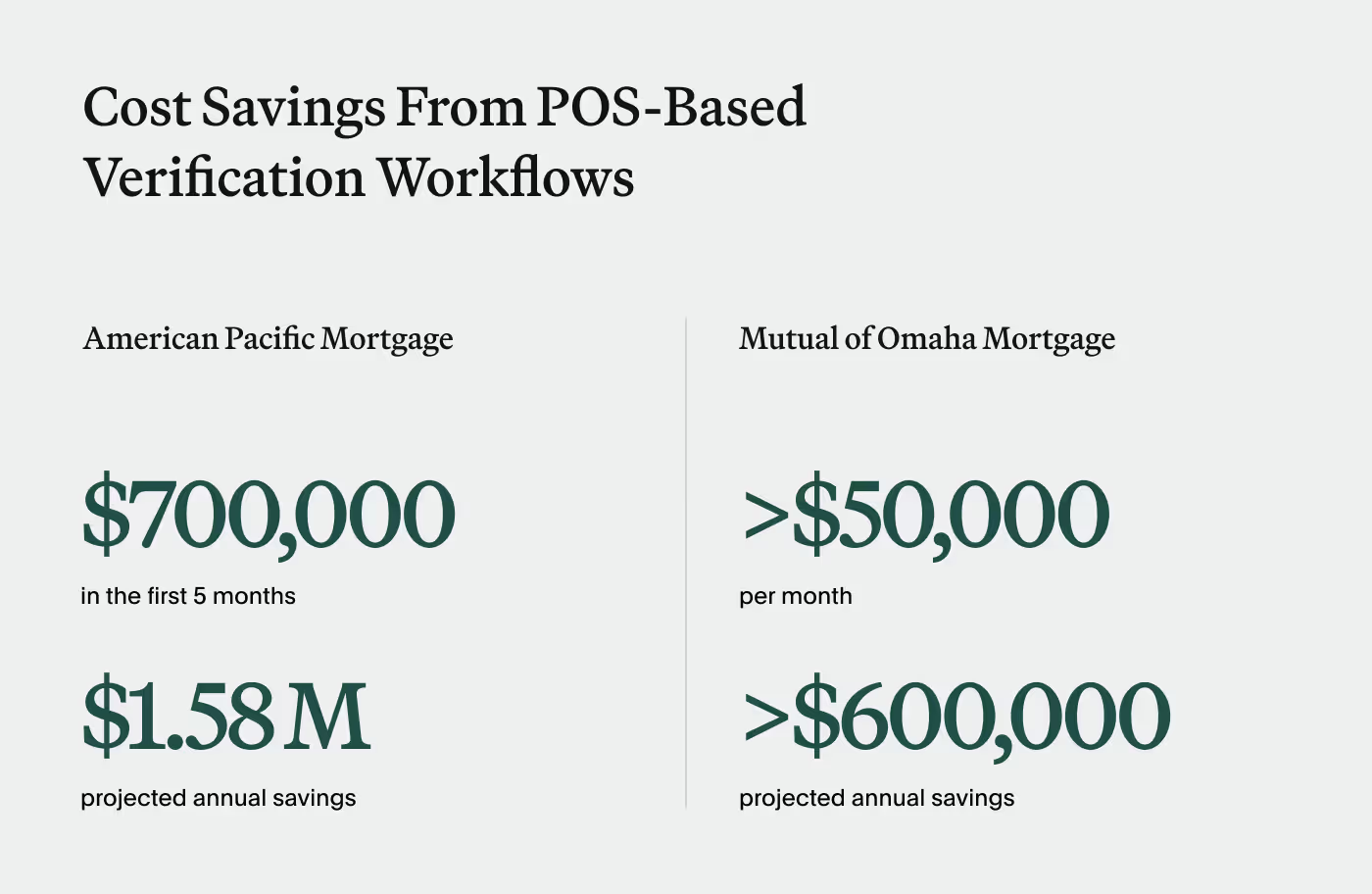

American Pacific Mortgage demonstrates the power of this approach. After embedding Argyle directly into their nCino POS system, they saved $700,000 in verification expenses in just five months, putting the company on pace for $1.58 million in annual savings.

Similarly, Mutual of Omaha Mortgage moved verifications to the POS and quickly saw impact. Their monthly savings now exceed $50,000—more than $600,000 annually. They have also sped up loan cycles since their processors now open files that already contain complete income and employment data, eliminating duplicate steps and manual uploads.

Must-have #3: real-time data for confident decisioning and accelerated timelines

Static verification reports are artifacts of an outdated era. In 2026, lenders need real-time, streaming data on income, employment, and assets—not snapshots that are obsolete before underwriting even begins.

Real-time verifications deliver critical advantages:

- They dramatically reduce fraud risk. With mortgage fraud indicators up 8.2% year-over-year in recent quarters, and income misrepresentation accounting for 46% of fraud cases investigated by Fannie Mae, the ability to verify income, employment, and assets directly from the source is essential fraud prevention.

- They provide instant insights into employment status changes, job transitions, and income fluctuations that could affect loan performance. If a borrower loses their job the day before applying for a mortgage loan, for example, real-time verifications will catch it. The same can’t be said for manual document collection and legacy verification databases, which offer data that can be weeks old.

- They accelerate cycle times by eliminating the delays inherent in traditional verification workflows. With real-time data access, information is available instantly when borrowers connect their accounts—no waiting or no follow-up requests. And when underwriting needs updated income, employment, and asset data before closing, real-time access means instant reverification. Traditional methods require restarting the request process, often adding a week or more to close times.

This speed advantage is particularly crucial in competitive markets where delays can cost lenders the deal. When American Pacific Mortgage implemented Argyle, they realized a 12.5-day reduction in cycle time—an advantage that translates directly to better borrower experiences and higher conversion rates.

Must-have #4: a unified verification waterfall

For lenders, verification provider fragmentation creates unnecessary complexity, inflated costs, and borrower friction. A single mortgage file might pass through The Work Number for employment verification, a separate vendor for asset verification, and yet another system for income validation.

Fragmentation also comes into play within verification types. If The Work Number doesn’t yield a hit for employment verification, for example, then the file typically gets passed through to another vendor or relegated to manual verification as a fallback. Each handoff introduces delay, each provider has different support processes, and the total cost adds up quickly.

The 2026 requirement is clear: a unified verification waterfall that performs multiple kinds of verification with built-in fallback options that can maximize borrower coverage. This cohesive approach minimizes manual intervention while maximizing automation across the entire verification spectrum.

Argyle was purpose-built to address this need. It offers verification of income (VOI), verification of employment (VOE), and verification of assets (VOA) through a single platform. It also offers automated fallbacks that use direct-source payroll data first followed by banking data if needed. And in cases where a direct data connection is not available, Argyle offers Doc VOI, an automated, document-based verification solutions that leverages optical character recognition (OCR) technology. In doing so, Argyle enables lenders to run their entire verification waterfall through one provider, driving more qualifications, less manual work, and higher conversion.

This unified approach means one integration, one support team, and one set of pricing across all verification types—dramatically simplifying operations while improving outcomes.

Must-have #5: GSE-approved, quality-assured verification reports

For mortgage lenders selling to Fannie Mae, Freddie Mac, or other investors, data quality and report structure aren't negotiable. Every verification report must meet strict GSE standards, present information in formats underwriters can quickly process, and maintain consistent quality regardless of data source.

Critical requirements include GSE-approved formats that meet Fannie Mae's Desktop Underwriter (DU) validation service and Freddie Mac's Loan Product Advisor asset and income modeler (AIM) standards. For instance, reports must clearly separate multiple employments to avoid confusion during underwriting. They need streamlined layouts designed specifically for underwriter workflow efficiency. And quality must remain consistent whether the verification draws from payroll, bank, or document data.

That’s why Argyle has gone to great lengths to be named an authorized report supplier for DU and AIM. The platform's recent report design upgrades ensure that our VOI, VOA, and Doc VOI verifications all meet the evolving standards lenders need for GSE compliance and representation and warranty relief.

Must-have #6: dramatic cost reduction through direct-source data

Because margins remain compressed across the mortgage industry, every dollar of operational expense is critically important. And verification costs have become a significant enough line item that lenders must actively manage this spend—yet many are still paying premium prices for inferior data.

Legacy database providers like The Work Number purchase consumer data and resell it at substantial markups, with costs that can spike to $200 per file when multiple borrowers or reverifications are involved.

Direct-source, consumer-permissioned verification providers like Argyle operate on a fundamentally different economic model. By connecting directly to payroll and banking systems with borrower permission, lenders access fresher, more complete data at a fraction of the cost—up to 80% less than legacy providers.

Argyle’s customers bear this out. Lake Michigan Credit Union saves $100 per loan with Argyle, and Alcova realized a 88% cost savings per loan. Beyond per-verification savings, the fact that Argyle offers POS-based verification workflows amplifies the economic benefit because more verifications qualify for GSE use.

Must-have #7: a borrower experience that matches 2026 expectations

Interest in more digital or fully digital mortgage processes has grown significantly in recent years and remains very high across all demographic groups, according to Fannie Mae. Recent homebuyers cite process acceleration (75%) and making the process easier (71%) as the top benefits of a digital mortgage experience. They expect mobile-friendly interfaces, instant responses, and zero-friction workflows that rival their experiences with fintech apps in other parts of their financial lives.

The traditional verification process fails this test spectacularly. It requires borrowers to hunt down paystubs and W-2s, upload documents that may be rejected for quality issues, and wait days or weeks for manual processing. Each friction point creates abandonment risk.

Embedded verification via direct-source, consumer-permissioned providers like Argyle transforms this experience. Borrowers simply connect to their payroll or banking accounts—credentials they already know—and verification happens instantly.

Argyle’s implementation options make this accessible for lenders of all sizes and technical capabilities. Leading LOS and POS systems offer prebuilt Argyle integrations, including Encompass, nCino, Consumer Connect, Tidalwave, The Big Point of Sale, Floify, Empower, and Byte. For lenders who want more control, Argyle's API enables fully customized verification workflows.

[H2] What leading lenders will look like in 2026

Take a snapshot of the modern mortgage lender’s verification model, and you'll see several defining characteristics:

- Automated workflows with seamless interoperability between POS and LOS

- POS-driven verifications that engage borrowers early

- Real-time data access that enables confident decisions

- A united waterfall that curbs inefficiencies

- GSE-quality reports for every verification type

- Lower operational costs through direct-source data

- Superior borrower experiences that win in competitive markets

This isn't aspirational—it's becoming the baseline expectation. Lenders who haven't made this transition will find themselves at an increasingly severe competitive disadvantage as borrowers compare experiences and as the industry continues its relentless march toward digital-first operations.

How Argyle helps lenders future-proof their verification strategy

Argyle's comprehensive verification platform addresses every requirement outlined above through a unified solution that includes:

• Payroll-based verification (VOIE) provides direct access to income and employment data for 90% of the U.S. workforce, including traditional employees, gig workers, and federal employees.

• Banking-based verification (VOA/VOAI) powered by Mastercard's open finance technology, offering up to 24 months of transaction history, investment account access, and comprehensive cash-flow

• Document-based verification (Doc VOI) using optical character recognition to extract income data from uploaded paystubs and W-2s, with direct integration to Freddie Mac's AIM Check for automated assessment.

• Comprehensive reporting and API datasets delivering GSE-approved reports alongside raw data access for lenders who want to build custom experiences.

Argyle integrates seamlessly with leading mortgage technology systems, ensuring smooth implementation and workflow continuity. And every customer receives dedicated support from experts who understand mortgage workflows—not generic help desk responses, but specialized guidance from a team that knows your operational challenges.

Ready to improve your verification infrastructure?

The mortgage market in 2026 belongs to lenders who embrace modern verification workflows.

Explore the Argyle platform to see how automated, embedded, real-time verification can transform your operations, or schedule a demo to see the platform in action and discuss your specific verification challenges with our team.